The Creator Economy

For over 600 years, innovations spawned new forms of entertainment. The printing press (invented around 1436) unleashed book publishing. Later, radio and movies (1895), TV (1927), and video games (1958) sprung onto the scene. However, amidst all this innovation, one thing remained constant: Content creation was both curated and centralized.

With the advent of the internet and smartphones, social media was born. For the first time, content creation was no longer centralized. It was distributed. As such, gatekeepers — like studio heads or masthead editors — were no longer required. Crucially, however, social media platforms — like Meta or TikTok — did not share the spoils with the content creators. They kept all the revenues for themselves.

This is beginning to change. Across industries — publishing, podcasting, esports, and education — content creators are finding ways to monetize their content directly with their fans. This new ecosystem is often called the creator economy. While it barely existed five years ago, today there are over 120 million content creators. In 2022, we expect the creator economy to generate about $60 billion of revenue per year with ~9% growth per year through 2024 when it may approach $75 billion of revenue. Around half of the revenues stem from ad-based video platforms, like YouTube. The other half is spread across a wide array of industries: publishing, education, and podcasting, among others.

The creators do need help, and platforms can assist. However, the platforms charge fees that can vary from less than 10% of creator’s revenues (Patreon, Spotify, and Unity) to as high nearly 85% (Roblox). The variance often depends on the value the platform provides across five functions: (1) creation, (2) hosting, (3) distribution, (4) promotion, and (5) monetization. The more functions these platforms perform, the higher the fees.

Today, the creator economy is diverse, vibrant, and growing. However, across many of the creator economy platforms, a similar pattern emerges. The lion’s share of the revenue is captured by a very small portion of the content creators. Far more than 80% of the revenues are created by far fewer than 20% of the creators. In short, the Pareto principle, or 80/20 rule, does not apply. The creator economy is “winner takes most.”

Going forward, we think there are three areas worth watching. First, traditional social media firms may begin to share some of the spoils with content creators. That is, platforms like Twitter may begin to emulate YouTube’s business model. Or, as Instagram and Facebook push further into e-commerce, they will create opportunities for content creators to share in the economic spoils.

Second, Web 3.0 may create opportunities for creator economy platforms to leverage augmented reality, blockchain, crypto, and NFTs to alter the economics of the creator economy. These tools can help facilitate a direct relationship between content creators and fans with a diminished role for digital intermediaries. In short, Web 3.0 may help improve the economics of content creators.

Third, artificial intelligence may alter the creator economy in several ways including by helping with content creation and helping brands find the right influencer or helping consumer find the right content. It will be interesting to watch. With that, let’s dig into the details.

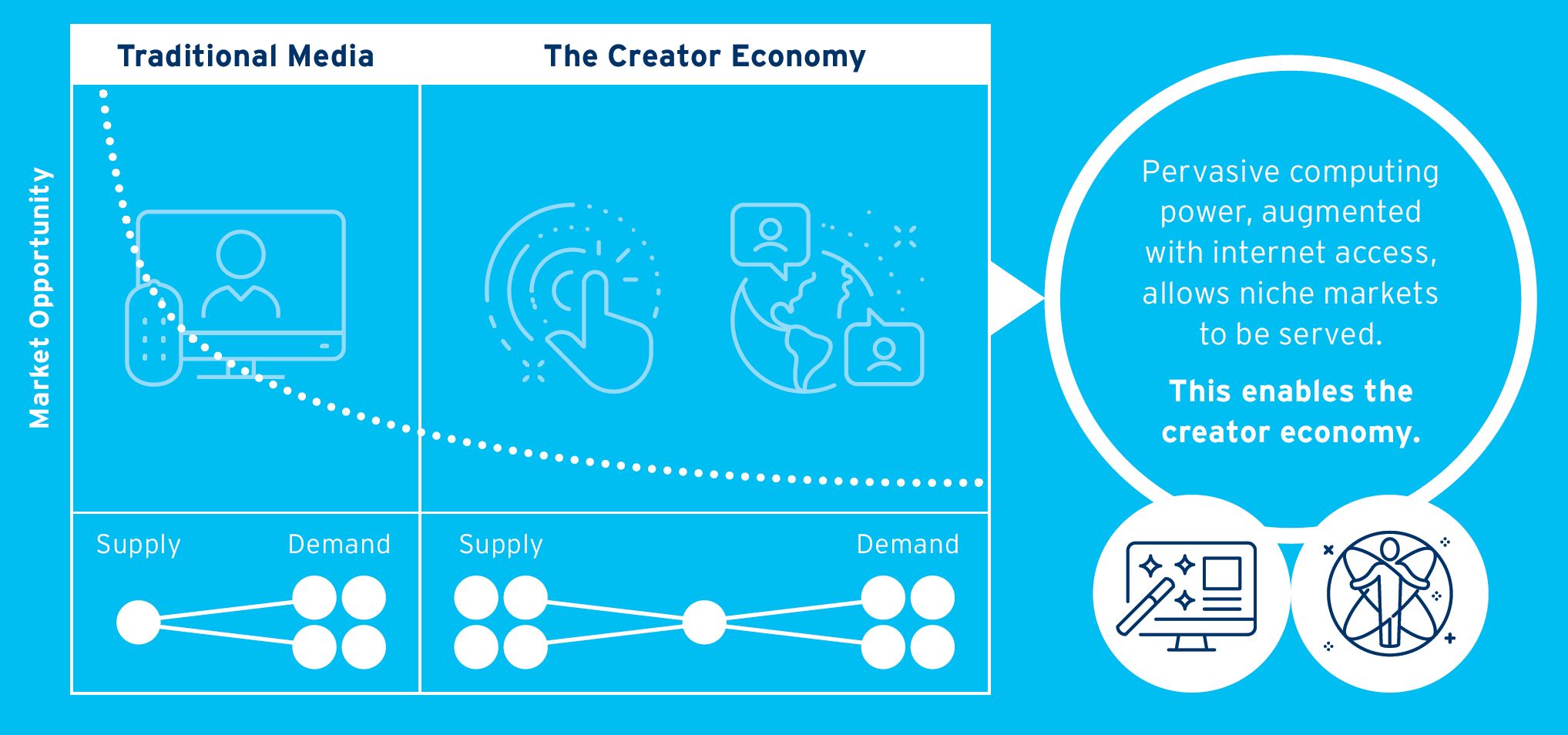

From Central to Distributed

The rise of the internet and smartphones has shifted the supply of entertainment from being centrally produced to a distributed model. This means creators are no longer focusing on the largest, most lucrative markets but instead can serve micro-markets and niches, leading to a “creator economy.”

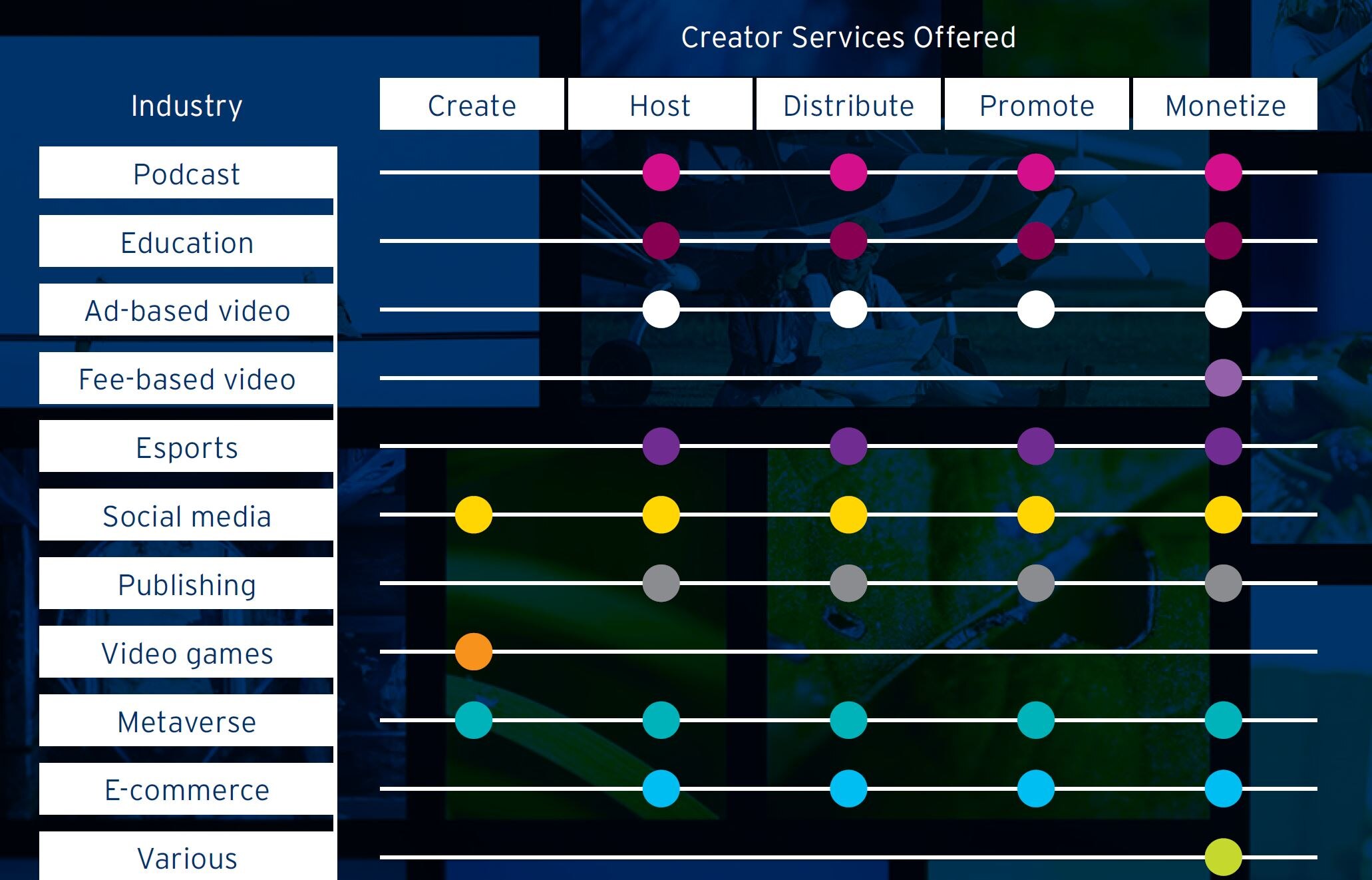

Creator Utilize Services to Generate Revenue

Monetization in the creator economy comes from ads, subscriptions, donations, purchases, and sponsorship. The generate revenues, creators need help and often use large platform so assist in creation, hosting, distribution, promotion, and monetization.

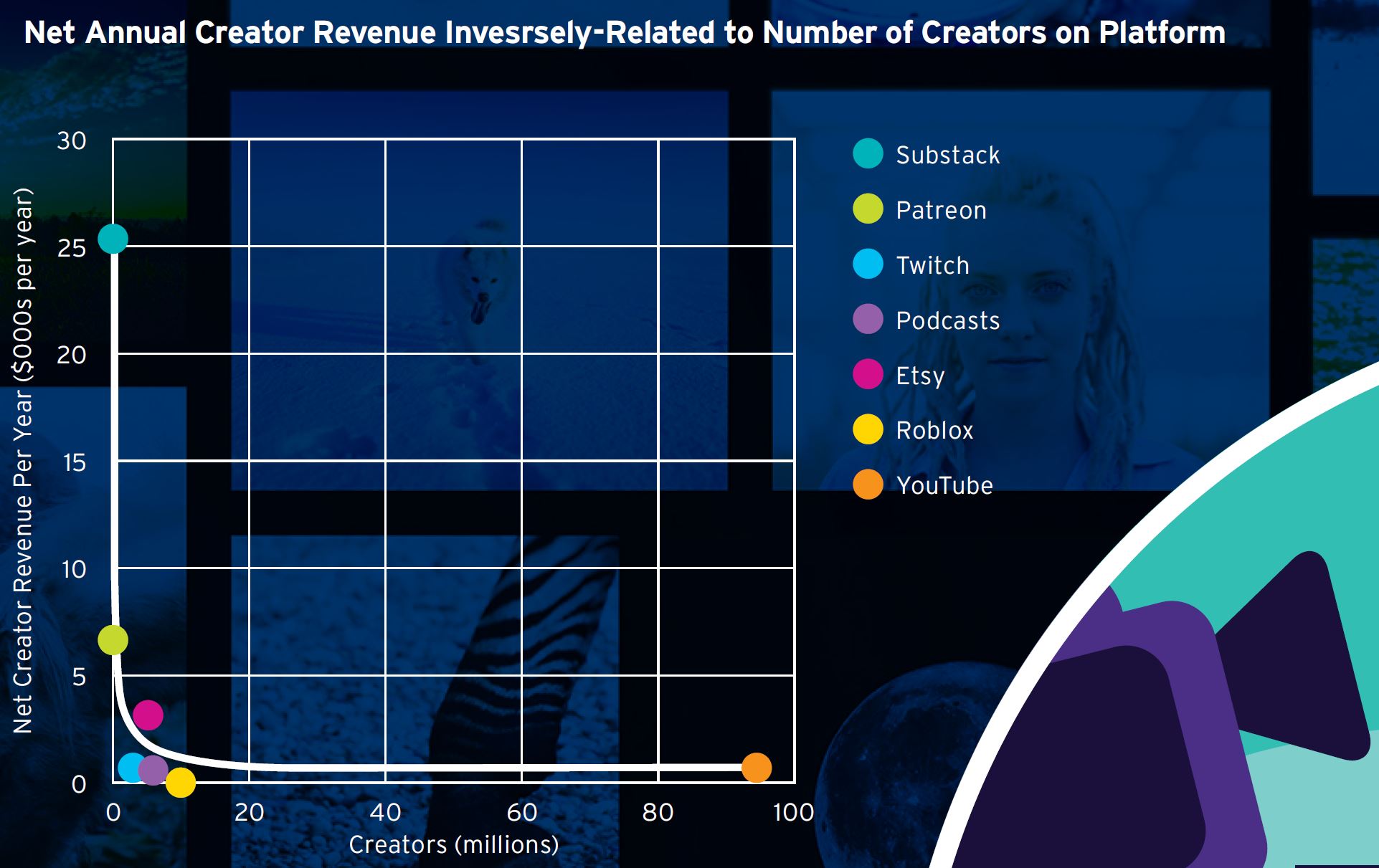

Winner Takes Most

Services fees charged for creator services vary greatly by platform. A creator’s average net revenue is inversely proportional to the number of creators that use that platform, making the creator economy highly concentrated.

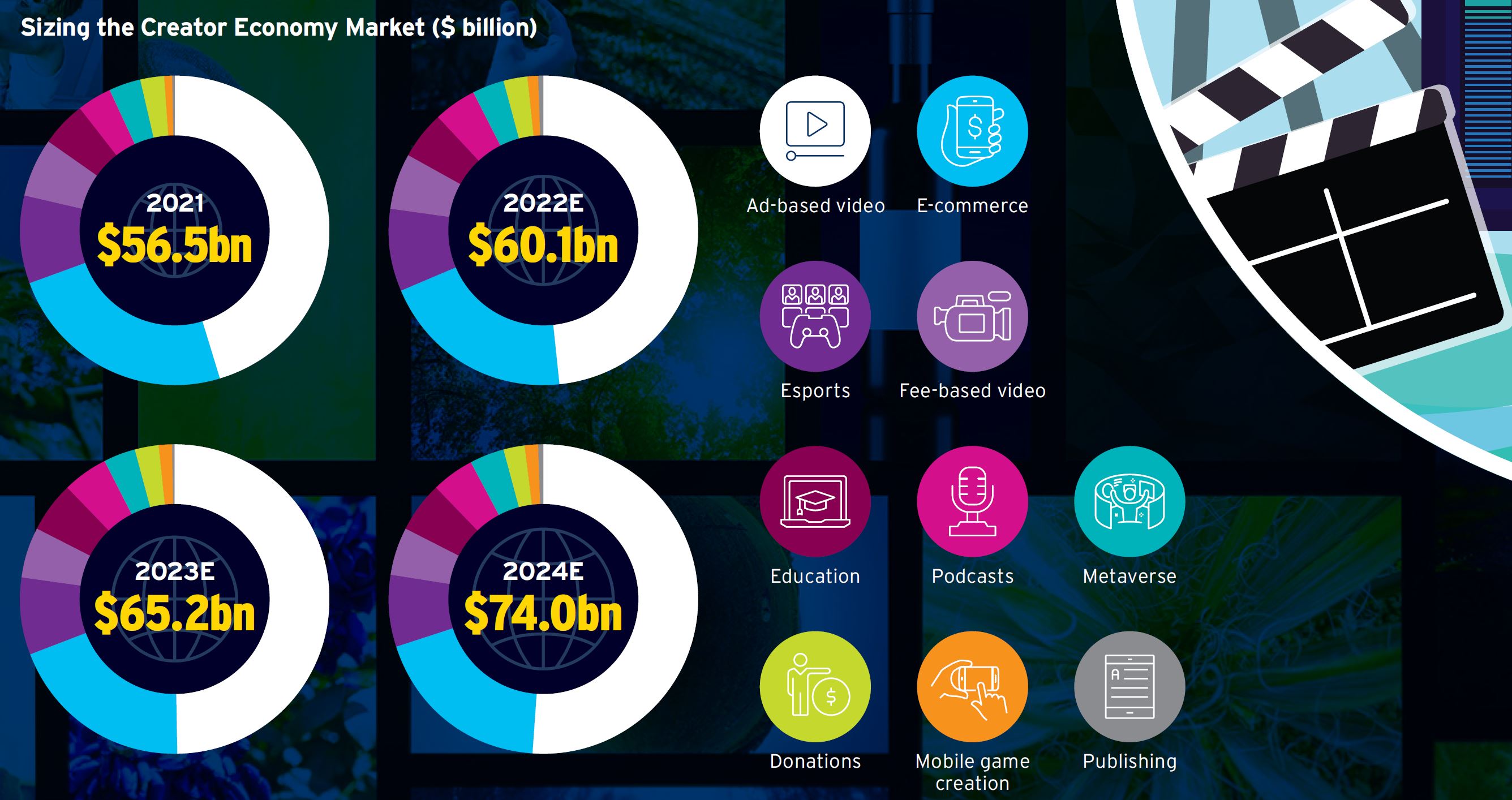

Sizing the Creator Economy

The market for the creator economy is currently around $60 billion per year and should grow nearly 9% through 2024, when it should approach $75 billion. The largest segment of the creator economy is ad-based video. Some segments of the market — podcasts, education, mobile games, Metaverse, and publishing — are poised to grow 20% or more per year.

Related Stories

Sign up to receive the latest insights from Citi.