North America Steel: Lessons from Trump 1.0, Expectations for Trump 2.0

Steel equities rallied sharply after Trump’s victory as investors anticipate potentially higher tariffs. But here’s a lesson we learned from Trump 1.0 to keep in mind as Trump 2.0 approaches: Buy the headlines on tariffs, but sell the implementation unless you’re bullish on demand. That’s the key conclusion of a new Citi Research report from metals and mining analyst Alexander Hacking that looks at what happened to steel prices during the first Trump presidency with an eye on potential policies in the second Trump presidency.

The U.S. steel industry is currently supported by a two-pronged tariff system. Antidumping and Countervailing Duties (AD/CVD) began to be assessed under President Obama and continued under Presidents Trump and Biden. Section 232 tariffs can be imposed for national-security reasons; the tariff is a blanket 25% on all types of steel.

Trump implemented Section 232 of the U.S. Trade Expansion Act in March 2018, more than a year after he became president. Countries including Japan, South Korea and Brazil, as well as the EU, negotiated a quota-tariff where tariffs were zero up to a quota; Canada and Mexico had no quota but were expected to avoid surges.

U.S. steel imports peaked at 40 million metric tons in 2014 as Chinese steel exports were surging. A series of AD/CVD cases under Obama reduced imports to 30 million tons, as most Chinese flat-rolled products (a type of processed steel that’s rolled into flat, rectangular sheets or strips) came with tariffs above 250%. Trump’s Section 232 implementation reduced the level further to 25 million tons. Imports rose again in 2022 as U.S. prices surged, offering a huge premium over the rest of the world.

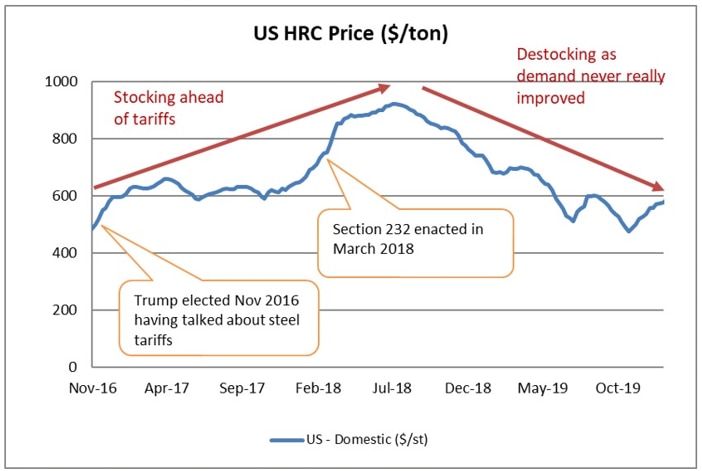

Steel prices doubled from $500 a short ton in November 2016, when Trump was elected, to $1,000 a short ton in August 2018 as apparent demand improved. But in hindsight, this runup included a relevant amount of restocking. That’s no surprise, as buyers are likely to buy more and not less when they read headlines about significant new import tariffs.

Steel demand rolled over starting in late 2018, exacerbated by stocking, and steel prices fell back to the neighborhood of $500 a ton by the end of 2019.

US HRC Price - Trump 1.0

© 2024 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research

It’s hard to see evidence that steel demand improved under Trump 1.0, and ultimately, it’s steel demand that’s been the bigger driver of prices, not tariffs. U.S. steel prices have consistently traded down to the cost of production during periods of weak demand, regardless of tariffs, while tariffs have exacerbated the price upside during periods of strong demand.

So what can we expect from Trump 2.0?

We note that Trump hasn’t offered specific proposals about steel tariffs, but could complement 10% tariffs on all products. If that applied to steel, it would boost the cost of some 80% of U.S. imports that currently arrive tariff-free from trade allies. This would support higher steel prices through the cycle, but we doubt it would change the fundamental demand dynamic described above.

The key question for Trump 2.0 is whether steel demand will improve. It’s hard to see any Trump 2.0 policy that will help steel demand in the short term, but lower Fed interest rates will likely support more construction activity and the Biden infrastructure bill may boost steel demand under Trump despite being disappointing in that respect so far.

Our new report, North America Steel: Lessons From Trump 1.0; Expectations for Trump 2.0, is available in full to existing Citi Research clients here.

Sign up to receive the latest insights from Citi.