Historically cargo has been used to supplement revenue but with the reverse in passenger demand, many operators are now looking at freight to generate an increased proportion of revenue and to minimize cash burn. Pre-COVID, approximately half of air freight was carried in the belly of passenger planes. The sudden fall in cargo capacity from the collapse in long-haul passenger travel and the rapid growth in cargo demand driven by PPE and packages have put a premium on cargo flights.

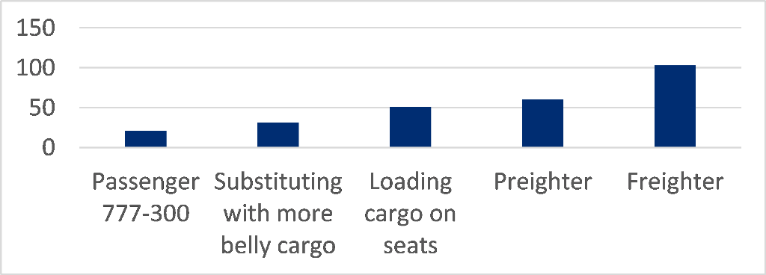

IATA estimate c.2500 passenger planes have been converted in the last year (to some extent) to accommodate in-cabin cargo. There are three main ways that operators have achieved this: (1) substituting passengers for more belly freight, (2) loading cargo onto seats or (3) converting to ‘preighters’ – i.e., removing seats for cargo.

Pavan and Charles have looked at the profitability model for the various options and have concluded ‘that ‘preighters’ start to make positive operating profits for the cargo routes that are priced above $4 per kg.’ They are cheaper and quicker than a full freighter conversion and although they cannot carry as much weight they offer more in terms of long-term flexibility as the conversion is temporary.

Figure 1: Cargo capacity for the various options for a 777-300

Source: Citi Research

Figure 2: Operating profit per flight sensitivity for a 777-300 passenger aircraft being utilized for freight operations through the three different options

Source: Citi Research

For more information on this subject, please see Aerospace, Airlines and Shipping: A Primer on ‘Preighters’ & Increasing Aircraft Cargo Capacity.

CGI is Citi’s premier non-independent thought leadership curation. It is not investment research. The comments expressed herein are summaries and/or views on selected thematic content from a Citi Research report. For the full CGI disclosure click here.