My Account

In February 2023, the SEC confirmed that T+1 would go live on May 28, 2024. The implementation of T+1 could potentially be quite complicated, as it will force market participants into making material adjustments to their existing operating models and underlying technology systems. With T+1’s deadline rapidly approaching in the US, the window for preparations is getting narrower.

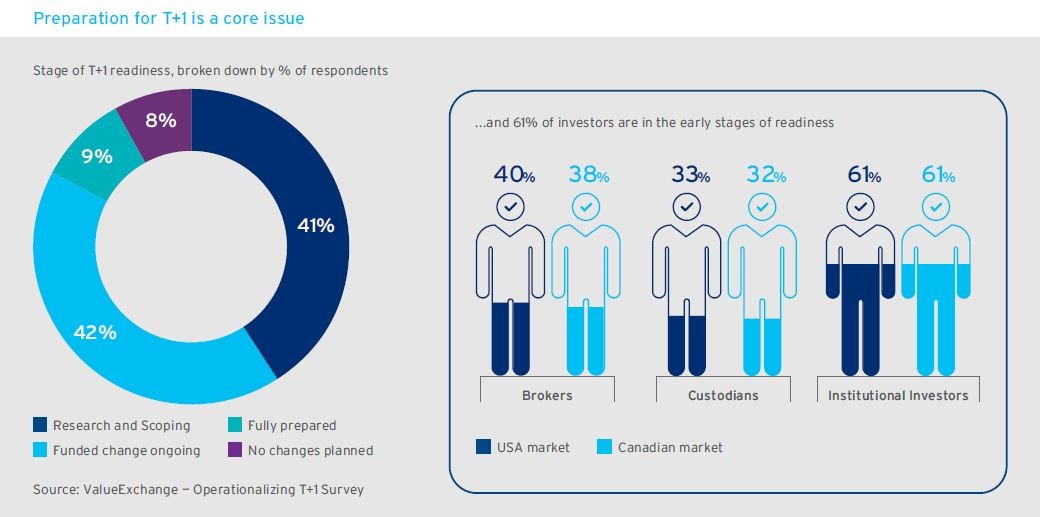

Industry preparations reveal a growing chasm

With the implementation date now finalized, market participant firms are actively working towards readiness though the levels of preparation among financial institutions appears to be quite varied. “The move to a T+1 settlement cycle has been an ongoing industry effort for more than two years now. However, we still see people in different pockets, namely those who are very prepared and ahead of the game, versus those who are much further behind, and are not yet thinking about the changes,” said Michele Hillery, Global Manager of Equity Clearing and DTC Settlement Service at DTCC.

For instance, the ValueExchange — Operationalizing T+1 survey found that 41% of the market still has not yet started planning for T+1. The survey further highlighted that institutional investors appear to be more advanced in their T+1 preparations compared to brokers and custodians3.

An institution’s size is also a decisive factor determining their levels of T+1 planning. “A large broker dealer for instance, is more likely to be compliant with the rules, having already embarked on the T+1 change journey. In contrast, a small broker dealer — which is still reliant on conducting their operations through fax — will probably have a bit more work to do. Budgetary constraints at smaller financial institutions may also be hampering their T+1 efforts,” explained Michele Pitts, Head of NAM Custody Product Management Strategic Initiatives at Citi.

Lou Rosato, Director of Global Investment Operations at BlackRock, shared that the $10 trillion asset manager is currently in the later stages of its T+1 planning. “We have a deep understanding and alignment on the changes that need to happen and have identified key focus areas for a firmwide and unified project with our custodians and brokers. Our formal engagement and planning began in 2022 and it is now ramping up this year,” noted Rosato.

Although major institutions with substantial operations in the US understand the full implications of the T+1 move, many outside of North America are still digesting the potential changes. For instance, the ValueExchange study found that not a single Asia-Pacific based financial institution was executing their T+1 plans, nor had anyone in the region even developed a concrete T+1 project funding request4. The study also revealed that 43% of Asia-Pacific based financial institutions were still in the research and information gathering stages of their T+1 planning efforts, versus 27% of those in Europe and 17% in the US5.

“The most significant impact is likely to be felt at buy and sell-side firms in Asia and Europe. They will need to make substantial changes to their operating, treasury and client service models to support their client trading in a compressed settlement environment. They will experience the most significant impact, but in many respects are the least prepared and have the most work still to do,” said Bryan Murphy, Global Head of Banks Sales, Securities Services, Citi.

By shortening the settlement cycle from T+2 to T+1, market participants trading US equities will have much less time between trading and the start of the settlement cycle to perform post-trade processing6. As things currently stand under the T+2 model in the US, the trade allocation and affirmation process takes place at 1130AM Eastern Time (ET) on T+1. Following the introduction of T+1, trade allocations will be brought forward to 0700PM ET on trade date, with a 0900PM ET on trade date cut-off for affirmations.

The diagram also highlights the timing challenges facing financial institutions operating in Europe and Asia-Pacific as it relates to allocations, affirmations and securities lending transactions. As the diagram shows, implementation of T+1 will mean financial institutions will have 16.5 hours less time to process allocations; 14.5 hours less time to process affirmations; and 18 hours less time to process securities lending transactions.

What are some of the operational challenges market participants will be facing? And how can financial institutions navigate the T+1? Click the full report to find out.

1 Citi – Securities Services Evolution 2022

2 DTCC – FAQs

3 ValueExchange – Operationalizing T+1

4 ValueExchange – Operationalizing T+1

5 ValueExchange – Operationalizing T+1

6 AFME – September 2022 – T+1 Settlement in Europe: Potential benefits and challenges

Related Stories

Securities Services

Get in Touch

Sign up to receive the latest insights from Citi.