My Account

Securities Services Evolution 2021

Article • October 08, 2021

Disruption and transformation in financial market infrastructures

The securities industry is on the brink of transformational change. New technologies and digitization look set to usher in not just greater consistency and efficiency, but also completely new asset types and trading opportunities. This in turn calls for greater collaboration among market participants, regulators and FMIs which will ultimately streamline processes and mitigate potential risks.

FMIs

A total of 15 leading FMIs (12 traditional, 3 non-traditional) participated in one-on-one in depth interviews which took place between 28 July and August 19 2021. Traditional FMIs interviewed included exchanges, centralized securities depositories and clearing houses. Non-traditional FMIs interviewed included a digital exchange, a digital asset custodian and a fintech.

Market participants

In order to gauge the sentiment of market participants across the industry, Citi Securities Services collaborated with Global Custodian to survey almost 400 individuals around the globe via an online poll that ran between 3 August and 1 September 2021. These included, among others, a broad mix of custodians, banks, broker dealers, asset managers and institutional investors

Executive Summary

The global securities landscape is on the verge of transformation, with new technologies and digitalization efforts poised to deliver major efficiencies and potential savings. This represents a radical change for an industry historically fragmented in terms of technology, operating models and process inconsistencies. The periodic volatility and remote working caused by the pandemic have been a catalyst for this change.

The pandemic has also highlighted the need for market participants, regulators and financial market infrastructures (FMIs)to co-operate on key initiatives, such as digitization and digitalization.1 Appetite for both is clearly increasing as their potential to transform the industry becomes more widely acknowledged by market participants and FMIs alike.

In the early days of the pandemic, high market volatility and volume underlined the critical role that FMIs and securities services providers play. The focus now is on how increased automation can deliver even greater resilience and efficiency, while simultaneously reducing risks and costs.

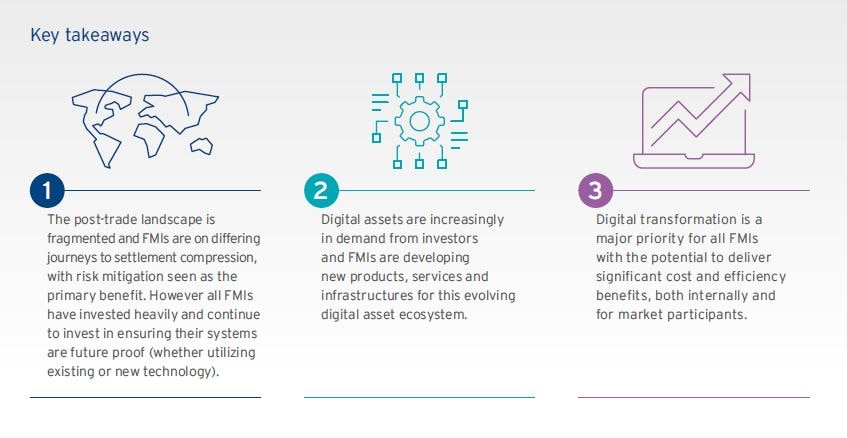

Settlement compression

Against this backdrop, settlement compression has once again become an important consideration for all involved, along with the associated trends of digital assets, technology and digital transformation. All these are now attracting attention and investment from the FMIs interviewed for this paper, as well as considerable interest from the market participants surveyed. The forthcoming shortening of the US settlement cycle to T+1 is one reason for this growing interest, recent periods of high volatility another. FMIs see the major benefit of reducing settlement cycles as risk reduction, which will in turn enable lower margin requirements and the release of capital that can be more efficiently deployed elsewhere. For example, most FMIs felt that some of this capital could be used to fund more trading activity, thus driving better liquidity. However, while most FMIs felt that these gains would apply to T+1, they would not apply to T+0 or atomic settlement because of the loss of netting benefits and the need to fund gross settlement. Although this is clearly an area of growing interest, there has not been much pressure from market participants to shorten settlement cycles, though this will probably change as nearly half of the market participants surveyed expect T+1 to arrive within the next five years.

When they transitioned from T+3 to T+2, some FMIs invested in technology that would allow them to handle any future shortening of the settlement cycle. As such, they did not view technology as a barrier for settlement compression, whereas almost 50% of market participants indicated that upgrading legacy technology would be key. Instead, FMIs felt that business process efficiency and the alignment of processes

among participants posed far greater challenges, noting that these had also been demanding during the previous transition.

Other topics discussed included the duration of operating hours and alignment with cash settlement systems. Neither FMIs nor market participants saw these as potential roadblocks to settlement compression and some FMIs have already instituted additional intraday settlement cycles to preclude any such issues. However, several Asian FMIs observed that time zone differences might make it difficult for US and European investors to source FX cost-effectively.

Digitalization

The biggest opportunities to transform our industry however, lie in digitization, digitalization and digital transformation. The market is responding in various ways: market participants and FMIs are actively participating or exploring use cases in digital assets, distributed ledger technology (DLT), digital asset initiatives,2 tokenization and fractionalization. In the case of FMIs, these were primarily for traditional assets, but they stressed the wider possibilities of using digital assets for less liquid markets, such as real estate or art.

The appropriate legal and regulatory infrastructure was also seen as absolutely critical to the success of digital assets, not just on a per country basis but also collaboratively and ultimately globally. Without this, many of the potential benefits and efficiencies could be lost. This view on regulation also applied to the success of atomic settlement, particularly in the context of creating a global settlement layer that would support all asset types with fungibility. On the future use of atomic settlement, both FMIs and market

participants were positive, with market participants slightly more optimistic on the timeline to production.

As the industry responds to these changing dynamics, it must do so in a way that does not compromise existing services. The ability to service both ‘old’ and ‘new’ assets will be essential. In the short term, most FMIs favored separation between their existing and any new infrastructures for traditional and digital assets, while acknowledging that integration was probably ideal in the longer term.

Technology and digital transformation

The FMIs interviewed were also pragmatic about how DLT could be applied to solve their real-world challenges. While a DLT-based market infrastructure was viewed positively by both FMIs and market participants in terms of efficiency and cost reduction, the FMIs were less convinced that DLT was key to shorter settlement cycles. They also saw DLT as being a challenging technology to implement, partly due to a lack of large-scale precedent in traditional markets and partly as a result of the absence of a dominant set of common standards. Other technologies such as artificial intelligence (AI) and machine learning (ML) are already being deployed by FMIs for market surveillance activities or to gain internal efficiencies. There is further potential for both technologies, especially in conjunction with DLT, in areas such as reducing

settlement fails and risk-adjusted trade pricing.

It is clear that new technologies are redefining the future of post-trade but this evolution will not take place overnight. The insights from this whitepaper reveal a post-trade environment that is complex and full of innovation and activity. Technology adoption continues apace and there is clearly a strong focus on speed, efficiency and supporting an extension of asset classes, while simultaneously minimizing risks and costs.

Securities Services

Get in Touch

Sign up to receive the latest news from Citi.