Semiconductors are in the spotlight of the tech rivalry between China and the U.S.

More specifically, Integrated Circuits (ICs) are coming into sharp focus.

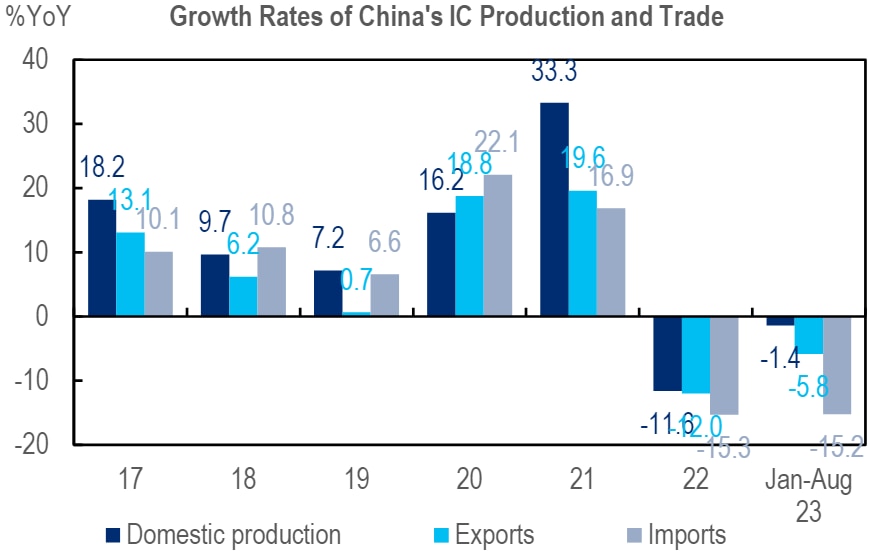

China has seen sharp declines in IC imports in the past two years, down -15.3%YoY in 2022 and another -15.2%YoY by number of units in Jan-Aug 2023.

From the peak of 637.9billion units in November 2021, the 12-month rolling sum of IC imports has lost a quarter to the latest 484.2billion as of August (see the first chart below). In the meantime, domestic production and exports of ICs have proved more resilient (see the second chart below).

The question is does that imply some progress in China on import substitution?

China saw sharp declines of IC imports in past two years in unit terms

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: China Customs, NBS, Haver Analytics, Citi Research

Domestic production and exports of ICs proved more resilient than imports

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: China Customs, Semiconductor Industry Association, Haver Analytics, Citi Research

China is the world’s largest semiconductor market, representing 31.4% of worldwide final sales or US$180billion out of US$574billion in 2022.

With a value of US$415.6bn, IC imports accounted for 15.3% of China’s total imports last year. It is still the largest import product for China, exceeding crude oil, which accounted for 13.5%.

The deficit of IC trade has almost doubled in the past decade to US$261.6bn in 2022, compared with headline trade surplus of US$857.3bn.

China’s semiconductor R&D push

Partly reacting to US tech bans, China’s government has put in place the “new whole-nation system” to spur its semiconductor to catch up with global competitors. That said, China’s

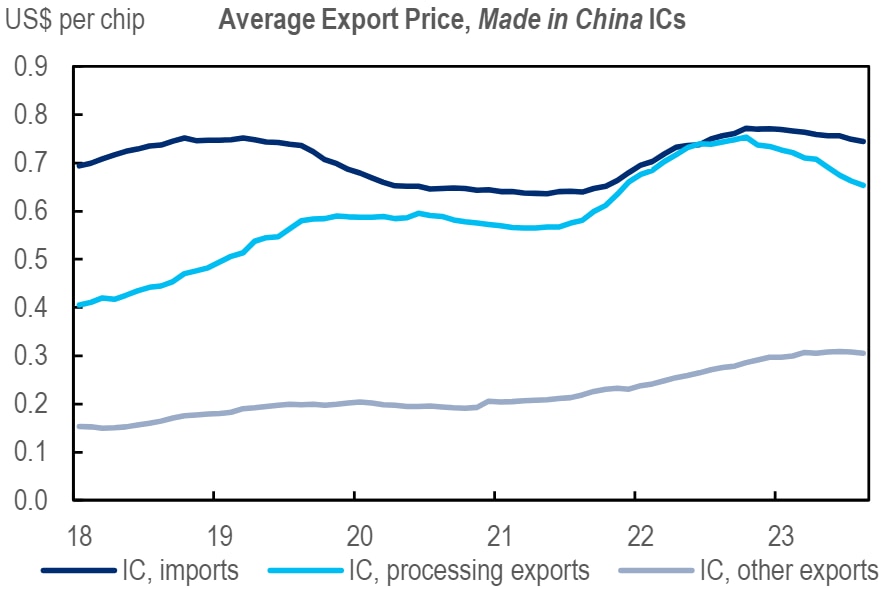

Processing trade contributed majority of China’s IC exports expansion

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Note: HS code 854231, 854232 and 854233. Data downloaded on Sep 26th.

Source: China Customs, Citi Research

R&D expenditure still lags well behind traditional powerhouses like the US, Taiwan and Korea (see the second chart below)

China is the world’s largest semiconductor market, representing 31.4% of worldwide chip sales in 2022

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: China Semiconductor Industry Association, Citi Research

China’s semiconductor R&D expenditure still behind traditional powerhouses (2022)

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Semiconductor Industry Association, Citi Research

Entrepreneurs and engineers are piling into the sector, on the back of the favourable policy environment and sheer size of the market. The number of newly registered semiconductor companies has been rising fast.

China is not exempt from global semiconductor cycles of course. China’s production of cell phones and computers dropped -3.8% and -18.4% in the 12 months until August. Its exports of them were down -12.3% and -23.2%, respectively.

As the world’s largest IC customer, China accounted for 36% of US semiconductor sales last year.

If breakthroughs are to be made through its substitution strategy, Chinese players have a good track record in driving the costs down and could be quite competitive at least in the home market, the Citi Research report said.

Moreover, the US semiconductor sector used to depend on a self-strengthening loop to maintain its technological lead: It channeled the high profits generated from business to R&D spending to ensure a comfortable lead ahead of rivals and dominance in the high-end segment of value chains.

The loss of the Chinese market could pose challenges to their business model. In addition, China could retaliate directly against US companies with penal measures of its own.

In short, the report says, the U.S. strategy could in fact strengthen Beijing’s determination to achieve tech self-reliance and could backfire on its own (U.S.) IC companies.

For more information on this subject, if you are a Velocity subscriber, please see the full report., first published on September 28th, here China Economics - Qualifying Import Substitution: The Semiconductor Case

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.